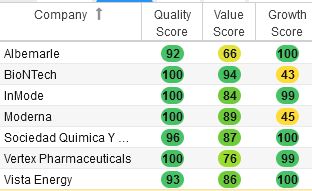

A stock that scores a perfect 10 should be on every investor’s list of stocks to buy. Any company that receives full marks on quality, value, or growth are stocks I’d considering a perfect 10. For this article, I’m using StockRover’s stock screening tool, which screens for such qualities among a very large basket of companies.

Despite many of these stocks to buy scoring so highly on one particular attribute, the market has heavily discounted most of these companies. Thus, it appears a tug-of-war between impatient investors and the Federal Reserve remains intact.

That said, there’s a lot to like about most of the companies on this list. These stocks to buy tend to have strong profitability and balance sheets. Other companies that earned a strong growth score posted a strong five-year historical performance in this category. These companies also tend to have solid forward EBITDA estimates for both revenue and earnings.

{kind=link}

In the table above, it’s clear that markets ignored drug manufacturers that posted strong profits from Covid vaccines. Investors should still earn steady profits, even if Covid becomes officially endemic in the next several years.

Additionally, lithium producers also find themselves on this list. For those who believe demand for lithium will rise in the next decade, there are a number of juicy stocks to buy here.

Let’s dive in.

| ALB | Albermarle | $283.90 |

| BNTX | BioNTech | $156.23 |

| INMD | InMode | $36.15 |

| MRNA | Moderna | $176.81 |

| SQM | Sociedad Química y Minera | $99.38 |

| VRTX | Vertex Pharmaceuticals | $316.16 |

| VIST | Vista Energy | $13.27 |

Albemarle (ALB)

Albemarle (NYSE:ALB) scored a perfect growth score on StockRover. The specialty chemicals manufacturing firm posted strong third-quarter net sales, reporting growth of 152% year-over-year to $2.1 billion.

One of the reasons for this growth score is the upside ALB stock provides investors from the global energy transition. Its lithium conversion plant in China and its Kemerton II expansion in Australia will bolster the company’s long-term growth prospects.

Albermarle acquired the Guangxi Tianyuan New Energy Materials in Quinzhou, China on Oct. 25 of this year. It’s expected the company will expand operations in the future. In addition, it has a project at Zhangjiagang. Since China is the largest lithium market in the world, Albermarle is strategically-positioned to supply the key input as demand grows.

Albermarle benefits from the incredible growth of the electric vehicle segment. Demand remains strong, despite near-term supply chain challenges. Still, once the seasonall- slow period ends this quarter, the company expects strong growth through next year.

EV investors should anticipate favorable government policies that strengthen the sector. As soon as the economy recovers, unit EV sales will rise, boosting ALB stock.

BioNTech (BNTX)

BioNTech (NASDAQ:BNTX) has a perfect quality stock grade, mainly due to attractive fundamentals. The vaccine maker reported positive clinical efficacy data against Omicron BA.4/BA.5. It said that its vaccine against that strain of Covid demonstrated an improved immune response. Additionally, the vaccine elicited a greater increase in neutralizing antibody titers than was anticipated.

BioNTech investors may assume that demand for the bivalent booster will increase. The flu season is underway, meaning the target market for patients seeking better protection against Omicron will result in a surge in requests for BioNTech’s vaccine.

In the last quarter, BioNTech posted a stark revenue decline of 43% year-over-year. Indeed, vaccine demand is lower compared to last year. Still, the company established flexible contracts for 2023. It will continue to fulfill those contracts in 2023 and beyond. Thus as the vibrant constantly evolves, BioNTech will continue to provide updates about the vaccine’s efficacy.

Governments everywhere could face the risk of a future variant evolving back to a deadlier disease. With the elderly especially at risk, I expect demand for the company’s vaccines will remain robust.

The kicker with BNTX stock is that this company trades at a price-to-earnings ratio in the low single digits.

InMode (INMD)

InMode (NASDAQ:INMD) makes laser and radiofrequency devices. Right now, I think the market is ignoring the perfect quality score for INMD stock.

In the third quarter, InMode posted revenue growth of nearly 30%. The company expects earnings per share of up to $2.30, above analyst consensus estimates.Indeed, despite the economy approaching a recession last quarter, InMode’s business did not slow down. I expect momentum to continue as patient bookings using the company’s devices grow.

InMode does not spend much on promoting its EmpowerRF product. To accelerate sales, the company will need to rely on doctors to recommend the treatment to their patients. Fortunately, InMode already has thousands of patients getting treatment. It has a disruptive product that has the potential to gain market share.

InMode engaged with larger institutions to raise awareness of its research efforts. This might help interest groups put pressure on insurance firms to provide reimbursement, thus boosting this company’s growth further.

Moderna (MRNA)

Moderna (NASDAQ:MRNA), like BioNTech, relies primarily on Covid vaccine sales for its revenue. In 2023, it will realize around $2 billion to $3 billion in deferred revenue. The sales deferral is a result of a delay in Moderna’s fill-finish operations.

Thus, I expect that in 2023, Moderna will report stronger revenue. As countries administer booster shots twice a year, I expect that the alignment of these shots with flu shots will boost demand. Over time, people will get used to taking a flu vaccine along with a Covid shot.

Moderna has $4.5 billion to $5.5 billion in contracted sales, excluding U.S. deals. Since it’s expected Moderna will deliver its product to Japan and the European Union, investors face limited geographical risks. Investors should look out for hospitalization rates rising during the winter season. To circumvent the risk of full emergency rooms at hospitals, governments are likely to encourage Covid vaccinations, with Moderna’s shot being among the top choices for most healthcare providers.

Moderna is also a company with a robust pipeline of products. The company is developing a personalized cancer vaccine. To succeed, it will need to offer treatment that is better than that of Merck’s (NYSE:MRK) Keytruda drug.

Sociedad Quimica Y Minera (SQM)

Sociedad Quimica Y Minera (NYSE:SQM) is a Chilean chemical company. It supplies plant nutrients, lithium, industrial chemicals, and iodine.

In the third quarter, SQM posted strong revenue as it earned $9.65 for the first nine months of 2022. This is sharply higher than the 92 cents of earnings per share reported in the same period last year. I think SQM will thrive as the demand for fertilizers remains strong. Still, as a cyclical firm, demand will fluctuate. Fortunately, farmers face tremendous pressure to obtain fertilizers to increase yields.

In the current quarter, SQM will continue expanding its lithium carbonate capacity in Chile, obtaining permits to increase its capacity. In the next two or three years, shareholders will benefit from the increased output. Given the company’s long-term price contracts, investors stand to benefit from lower volatility in revenue and earnings.

That said, spot prices for materials like hydrogen peroxide and lithium should rise in 2023. The market needs more supply, and demand is more likely to increase as the economy improves. That’s a nice setup for profitable growth for this agri supplier.

Vertex Pharmaceuticals (VRTX)

Vertex Pharmaceuticals (NASDAQ:VRTX) is on what appears to be a sustained uptrend. StockRover assigned a perfect quality score on VRTX stock because of its bright future.

I think Vertex is at a strategic inflection point. The company invested heavily in research and development, with will propel it to discover transformative medicines for serious diseases in specialty markets. As a small molecule company, Vertex has the tools to target specific diseases. For example, Trikafta is a cystic fibrosis drug that treats up to 90% of CF patients.

The company is developing treatments for five additional disease areas. Investors do not need to wait long for this company to reach the market. That’s because many of these treatments are in late-stage development. For example, it will have drugs that treat sickle cell disease and beta-thalassemia.

These drugs should impact the company’s fundamentals positively over the next year, making this stock a top pick on my list.

Vista Energy (VIST)

Vista Energy (NYSE:VIST) is another company that earned a perfect growth stock score. In the third quarter, the oil and gas firm posted revenue of $333.6 million, up more than 90% from last year.

Vista finished with around 54,000 barrels of oil per day in production. It’s expected the company will grow its production volumes by 15% to 20% annually. By 2026, Vista expects production to reach 80,000 barrels daily, though internally, the company has higher targets. To do so, the company will rely on the development of Aguada Federal and Bajada del Palo Oeste.

Vista is also expanding its infrastructure, including its OldelVal pipeline which is operating at full capacity. Still, there’s plenty of room for production increases to levels above what the market expects.

Vista has strong cash flow growth. To maximize shareholder returns, it could allocate its $2.5 billion in cash flow by 2026 through a buyback program. That’s partly because of the company’s front-end infrastructure commitments. This will result in higher production, increasing cash flow, and enabling Vista to pay down its debt. I like the way this stock is positioned right now.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.